My Sister Withdrew $500,000 from My Account and Went to Hawaii with My Mom. “Good Luck Starting Over,” She Texted. Three Days Later, They Called Me in a Panic and Asked, “Why Is the Money Frozen?” I Stayed Calm.

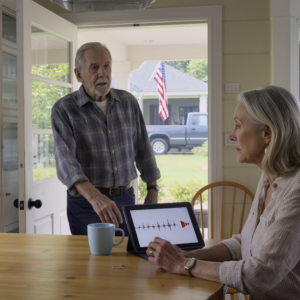

I was in D.C. for the Army Sustainment Symposium, the kind of conference where everyone wears a badge and talks about supply chains like they’re discussing baseball scores. I had my uniform pressed, my notes organized, and a full day of panels ahead of me. My phone vibrated once, then again. The subject line read, “Enjoy your new start.” It was from my mom.

I almost ignored it. My mother doesn’t usually email unless she’s forwarding something about blood pressure or a coupon that expired in 2019. But something about the wording made me open it. The message was short, three paragraphs. She and my sister Lauren had decided to start fresh. They had moved to Maui. The house was too heavy with memories. My savings had been handled, and I would be fine because I’ve always been good at landing on my feet.

That’s when my bank app pushed a notification. Wire transfer initiated: $487,320.

For a second, I stared at the number, not because I didn’t understand it. I understood it perfectly. That number was close enough to my total savings to make the point clear. I stepped out of line. The guy behind me sighed like I had personally ruined his morning. I walked outside, leaned against the brick wall, and opened the app fully.

Status: pending review.

That one phrase kept my pulse steady. If the transfer had already cleared, I would have seen completed. It didn’t say that. It said pending review. The destination bank was in Hawaii. I checked the timestamp. 6:58 a.m. Mountain time. They had done it less than an hour ago. My sister had drained my account and boarded a plane.

That’s the part most people focus on: the betrayal, the money, the Hawaii part. People love the Hawaii detail. It makes it sound like a movie. But at 7:45 a.m., I wasn’t thinking about palm trees. I was thinking about wire limits.

Eight months earlier, I had lowered my online transfer limit. I opened the transaction details. Only $63,000 had actually left the account. The rest was sitting in review, flagged because it exceeded my adjusted daily threshold and triggered a fraud alert I had placed months before. I didn’t feel rage. I didn’t feel panic. I felt confirmation.

I called the bank’s fraud line while walking back toward the hotel. A woman with a calm voice asked for verification details. I gave them. She confirmed the transfer was under manual review due to out-of-pattern activity. “Did you authorize this transaction?” she asked.

“No.”

She placed an immediate freeze on the account. She told me the receiving bank would be notified. She said someone from the fraud investigations team would contact me within two hours. I thanked her and ended the call.

Then my phone rang again. Lauren. I let it go to voicemail. Thirty seconds later, my mom called. I answered that one. Her voice wasn’t calm. It wasn’t steady. It was tight.

“Why isn’t the card working?” she asked.

“What card?” I said.

“The card for the rental.”

There it was. Maui wasn’t a dream. It was a short-term rental.

I walked back into the hotel lobby and sat down. People in suits moved around me. Someone was arguing about panel seating. Life was continuing at full volume.

“What rental?” I asked.

“The condo,” she said. “Lauren said everything went through.”

I opened my laptop and logged into the full banking portal. The wire had triggered a multi-layer review. My adjusted online limit blocked the majority of it. The fraud alert required voice confirmation before completion. They hadn’t gotten that confirmation.

“I didn’t authorize anything,” I said.

There was silence on the other end. Then Lauren’s voice cut in. She must have taken the phone.

“Why is the transfer frozen?” she demanded.

“Because I didn’t approve it.”

“You always approve big transfers,” she said. “You move money around all the time.”

That part almost made me laugh. Yes, I move money between brokerage accounts, between institutions, with documentation, with two-factor authentication, with intention.

“You don’t have authorization,” I said.

“It’s family money,” she snapped.

No, it wasn’t.

I ended the call before the conversation turned into something I would regret. Then I opened my security camera app. The moving truck had arrived at 8:52 a.m. Mountain time. The footage showed Lauren standing in the driveway with her hands on her hips, directing two movers. My mother carried out framed photos. The dining table I bought in 2020 disappeared into the truck. Electronics first. Boxes next. The safe in my bedroom was opened. They knew where it was. They took the emergency cash, $800. That part almost felt symbolic.

The camera audio picked up Lauren saying, “Take anything that’s worth something.” I paused the video and leaned back in the chair.

I wasn’t surprised.

That’s the part that sounds strange when I say it out loud. But surprise requires uncertainty. I didn’t have uncertainty anymore.

For eight months, I had been watching small things. Mail slightly misaligned after being resealed. Questions about daily wire limits. Lauren asking how long transfers take to settle. My mother hovering behind me when I paid the mortgage. One night in March, I found Lauren at my desk with a printed bank statement she had pulled from the recycle bin. She claimed she was just using the paper for scratch notes. Most people don’t use $500,000 balance summaries as scrap paper.

I didn’t confront them then. I documented.

Because here’s the reality: I’m an Army officer with a security clearance. Financial instability isn’t just personal. It’s professional. If something looked like fraud tied to my name, it wouldn’t just cost me money. It could cost me my career.

So I prepared quietly.

At 8:12 a.m., my phone buzzed again. Fraud case opened. I closed the banking portal, checked the time, and saw my first panel started in 20 minutes. I stood up, adjusted my jacket, and walked toward the conference hall. Lauren thought she had drained my account. She hadn’t. And the most important part wasn’t the money that got frozen. It was the documentation.

I kept my face neutral as I took my seat in the conference hall and opened my notebook like nothing in my personal life had just detonated. A colonel was explaining distribution timelines for forward units. Slides clicked. People typed. I wrote down exactly three words.

Check access history.

My father died two years before that morning in D.C. A stroke. Quick. No long hospital goodbye, just a phone call and a flight home. My mom had been married to him for 38 years. When he was gone, she said the house felt too quiet. She didn’t want to stay there alone.

I had just made captain. I had stable orders at Fort Carson. I had a house I bought in 2019 after my second deployment. It wasn’t huge. Three bedrooms, manageable mortgage, clean neighborhood. It made sense to let her move in. It also made sense to let my sister stay for a few months. Lauren was five years older than me. She had bounced between jobs and cities for most of her adult life. She called it being flexible. My mom called it finding herself. I called it expensive.

At the time, Lauren had just shut down a small online boutique that never really made money. She was behind on credit cards. She said she needed time to reset. A few months turned into a year, then two, then four. I covered the mortgage, utilities, property taxes, groceries, home insurance. I didn’t resent it at first. I was making good money for an officer with my time in service. I had deployment savings. I had invested steadily since I was a second lieutenant. My savings didn’t come from one lucky stock. It came from 12 years of not buying things I didn’t need.

My mom was added to a household expense account with limited access. It had a separate debit card. It was strictly for groceries and utilities. The main savings account was separate. Different bank, different login, different structure. Lauren didn’t have official access to anything. But access isn’t always formal. She lived in my house. She saw my mail. She saw when I logged in. She heard me mention account names in passing conversations. She had proximity.

The first red flag wasn’t dramatic. It was a piece of mail. I found a bank envelope on the kitchen counter that I was sure I hadn’t opened yet. The flap was slightly bent. Not torn, just imperfect. I didn’t say anything. A week later, another envelope looked resealed. Same pattern, slight misalignment. Humidity doesn’t reseal glue.

Then came the questions. Lauren asked how long transfers take to process. She framed it as curiosity. She said she was trying to understand financial systems better. She asked whether daily wire limits were per account or per person. She asked if military allotments worked like automatic bank drafts. The questions were specific, too specific.

One night in March, I came home from PT and found her sitting at my desk in the spare room I used as an office. She had a printed bank statement in front of her. It was one I had thrown into the recycle bin. She flipped it over when I walked in.

“Just using the paper,” she said.

The statement showed a balance of $512,438 at the time.

That’s when I stopped assuming coincidence.

My mom’s behavior shifted too. She started standing near me when I paid bills online. Not close enough to be obvious, close enough to glance at the screen. Her eyes didn’t land directly on the numbers. They hovered near them.

I tried something small. I logged into a different account one evening and said out loud that I was moving money around. I wasn’t. I just wanted to see if the topic resurfaced. The next day, Lauren asked, “How do you decide which account to use for big moves?”

It wasn’t paranoia if the pattern was consistent.

Still, I didn’t confront them. I didn’t sit everyone down for a dramatic family meeting. I didn’t threaten to kick anyone out. I watched. There’s a difference between suspicion and confirmation. I needed confirmation. I also needed to protect my career.

Financial issues are a clearance risk. Not because losing money automatically makes you unfit, but because instability makes people vulnerable, and vulnerability invites scrutiny. If something irregular happened with my accounts and I hadn’t documented prior concerns, it could look like negligence or worse.

I checked my online banking security logs. There were a few login attempts that didn’t match my device history. Nothing that resulted in access, just attempts. Different browser. Same IP address. My house.

I changed passwords quietly. I enabled two-factor authentication everywhere, quietly. I lowered my online wire limit, quietly. I called the bank and placed a precautionary fraud alert, framed as routine security tightening, quietly.

At dinner one evening, Lauren mentioned Hawaii out of nowhere. She said she’d always wanted to live somewhere warm. My mom said she’d love to wake up near the ocean. I asked how they’d afford it. Lauren waved a hand.

“We’ll figure it out.”

That phrase landed differently after the browser searches I’d seen.

Yes, I checked the shared tablet. It wasn’t locked. It was logged into my Wi-Fi. I wasn’t hacking anything. I was reviewing activity on a device in my house. Search history included: how to wire large amounts online, can you transfer money without authorization, bank wire limit workarounds.

That was enough.

I scheduled a consultation with a civilian attorney who specialized in financial disputes. I didn’t accuse anyone. I described patterns. I asked what protection looked like. He didn’t laugh. That mattered. He said documentation mattered more than confrontation. He said lowering limits was smart. He said if someone attempted unauthorized access and failed, that record would be valuable.

I went home that night and looked around my own living room. The couch I paid for. The dining table I assembled myself. The framed photo of my dad at my commissioning ceremony. My mom was watching television. Lauren was on her laptop. Nothing looked violent. Nothing looked criminal. It looked ordinary.

But ordinary is how most bad decisions start.

Back in the conference hall in D.C., the colonel wrapped up his briefing and opened the floor for questions. My phone buzzed again in my lap. Another fraud alert update. The transfer was still under review, and Lauren had just tried to initiate a second transaction.

I kept my phone face down on the conference table while the room filled with polite applause. A second transfer attempt meant one thing. This wasn’t panic. It was persistence.

I stepped into the hallway and opened the fraud alert notification. The amount was smaller this time: $24,900. Just under the threshold that typically triggers automatic reporting reviews at many institutions. That told me Lauren had done some reading. The status showed: declined, exceeds authorized access.

She was adjusting her strategy.

I didn’t call her. I didn’t text. I called the bank again. The fraud specialist confirmed two separate attempts within 30 minutes. Both initiated from a device tied to my home IP address. Both flagged due to limit restrictions and voice-confirmation requirements.

“Has anyone else been added as an authorized user on your primary account?” the specialist asked.

“No.”

“Has anyone had physical access to your debit card or saved passwords?”

“Yes,” I said. “They live in my house.”

There was a pause. Not judgment, just documentation.

She placed an extended freeze on outbound wires and restricted online transfer capability until I could verify identity in person upon return. She also noted attempted access in the file.

That mattered more than the money.

I went back into the conference room and sat through the rest of the session like nothing was wrong. Years in the Army train you to compartmentalize. You can address one crisis without announcing it to the world. But my brain wasn’t on logistics anymore. It was running a timeline: mail tampering, specific questions, login attempts, wire limit searches, now multiple transfer attempts.

This wasn’t a misunderstanding. It was planning.

During lunch, I stepped outside and called my attorney. I explained the second attempt. He didn’t sound surprised.

“Good,” he said.

“Good?” I repeated.

“Good that it failed. Good that it’s documented. Every failed attempt builds intent.”

He asked whether anyone had power of attorney over my finances. The answer was no. I’ve never handed over financial control to anyone. That was non-negotiable. He asked whether my mother’s debit card was linked in any way to the primary savings account. It wasn’t. The household expense account was separate by design.

Then he asked something else. “Have you updated beneficiary information recently?”

I hadn’t thought about that. Beneficiary access doesn’t allow someone to transfer funds while you’re alive. But knowing who’s listed can shape someone’s assumptions about future access. I logged into my portal and confirmed everything was unchanged.

That afternoon, my phone lit up again. Lauren, then my mom, then Lauren again. I answered the third call.

“What did you change?” Lauren demanded.

“I secured my accounts.”

“You moved the money,” she said.

I didn’t respond immediately. Silence makes people talk more.

“You’ve been hiding funds,” she added. “That’s why it won’t go through.”

Hiding funds. The phrasing was interesting. It implied she expected the full balance to be available in that one account.

“It’s my account,” I said. “There’s nothing to hide.”

She exhaled sharply. “We already signed the lease.”

That was new information.

“How long is the lease?”

“A year.”

Maui rental rates aren’t small. A year commitment meant she was confident the transfer would clear.

“You shouldn’t sign contracts assuming access to money that isn’t yours,” I said.

“It’s family money,” she repeated.

“No, it wasn’t. It was deployment savings, housing allowances, reenlistment bonuses, and disciplined investing.”

Lauren hung up.

I texted my neighbor Greta back in Colorado and asked a simple question. “Did you see a moving truck at my place today?” She replied within minutes. Yes, large white truck. She thought I was remodeling. She had a short video clip from her Ring camera of Lauren directing movers in the driveway. I asked her to save it.

Evidence doesn’t always come from dramatic sources. Sometimes it comes from the neighbor who waters her plants at 8:00 a.m.

By midafternoon, my fraud case was officially escalated to internal investigations. The bank confirmed the receiving institution in Hawaii had been notified of the pending review and partial freeze. The $63,000 that initially left my account was now flagged on the receiving end. It wasn’t gone yet.

I scheduled an appointment at my bank branch in Colorado for the morning after I landed. In-person verification adds weight to fraud claims. Remote calls are helpful. Physical presence is stronger.

Before the final panel of the day, I stepped into a quiet corner and opened my security camera feed again. The house looked stripped. The dining table was gone. The television was gone. The cedar chest my father brought back from New Mexico years ago was gone. Lauren’s bedroom door was open, empty. I zoomed in on the safe location. The door hung slightly ajar. They hadn’t even bothered to close it properly. That detail annoyed me more than the money. Carelessness after calculated planning. It didn’t match.

I checked the timestamp again. The moving truck had left at 10:12 a.m. Mountain time. The second wire attempt was at 10:16 a.m. She was still inside the house when she tried again. The timing told me she believed proximity increased her chances of success. It didn’t.

At 4:30 p.m., my commander texted a group message reminding everyone about uniform standards for the formal dinner event that night. Normal life. Normal expectations. I texted back a thumbs up. Then I opened my banking portal one more time. The transfer status had changed to under extended review. That meant more eyes were on it now. Human eyes, not just algorithms.

Lauren called again as I stood in front of the hotel mirror, adjusting my dress uniform for the evening event. This time, her voice was different. Not angry, tight.

“They’re asking questions at the rental office,” she said. “About payment verification.”

“That makes sense,” I said.

“You need to fix this.”

I straightened my collar and looked at my reflection. “No,” I said. “I don’t.”

Silence filled the line. Then she asked the one question that confirmed everything.

“Whose account was that?”

I ended the call without answering.

I lowered my phone and walked into the formal dinner like nothing in my personal life had shifted. The ballroom was loud, full of officers and contractors making small talk over plated chicken. Someone laughed too hard at something about procurement timelines. I nodded at the right moments. I shook hands. I kept my voice steady. Inside, my mind was replaying one sentence.

Whose account was that?

Not why is the bank freezing it? Not can we fix this? But whose account?

Lauren believed there were multiple accounts. She believed there was money somewhere she hadn’t reached. That meant the preparation I started eight months earlier hadn’t just been smart. It had been necessary.

Eight months ago, after that night I caught her with my bank statement, I didn’t confront her. I didn’t threaten eviction. I didn’t start a fight. I started restructuring.

The first thing I did was move the bulk of my savings, about $420,000, into a separate brokerage institution under an account structure that required in-person verification for large withdrawals. Not because I expected immediate theft, because redundancy matters.

The second thing I did was lower my daily wire transfer limit online. Most people never touch that setting. It sits there quietly at a number that seems generous. I cut mine down dramatically. Then I enabled voice confirmation for outbound transfers above a set threshold. I also placed a fraud alert on the primary account, framed as a standard security upgrade.

None of that required drama. It required 10 minutes on the phone and basic awareness.

After that, I inventoried the house. I photographed electronics, recorded serial numbers, updated my homeowner’s insurance rider to reflect current value. I didn’t tell anyone. I also removed my mom’s debit card from automatic overdraft backup. The household expense account remained active, but it was capped and isolated. It couldn’t cascade into savings.

Every change I made was small on its own. Together, they created friction. Lauren never noticed the friction building. She only noticed when it stopped her.

Back in D.C., I stepped outside the hotel after dinner and called my attorney again. I told him about the second attempt and her question about the account. He was quiet for a moment.

“That question tells me she believed she was accessing your entire liquid position,” he said.

“She wasn’t.”

“Good.”

He explained something I already understood but needed to hear out loud. Intent matters. Repeated attempts matter. Communication acknowledging expectation of access matters.

The email from my mother — Enjoy your new start — was already saved in multiple places. I forwarded it to him. I downloaded a copy. I saved it to cloud storage. Documentation doesn’t argue. It sits quietly and waits.

The next morning, before my flight home, the bank’s fraud investigations unit called. They confirmed the receiving institution in Hawaii had placed a temporary hold on the $63,000 that initially cleared. It had not been fully released due to the originating bank’s fraud escalation.

“Is there any possibility this was authorized by a joint account holder?” the investigator asked.

“No joint holders,” I said. “No power of attorney. No written authorization.”

“Understood.”

They told me the review process could take several days, possibly longer if law enforcement became involved. I didn’t rush that part.

On the flight back to Colorado, I didn’t sleep. I reviewed my notes instead. Dates, times, screenshots, login-attempt logs. There were three unsuccessful login attempts from my home IP address two weeks earlier, all from a browser I don’t use. That wasn’t coincidence.

When we landed in Denver, my phone reconnected to the network and buzzed repeatedly. Missed calls. Voicemails. Texts. Lauren’s last message read: Call me. We need to fix this.

Fix what? Fix the assumption that my savings were communal property? Fix the belief that discipline is optional?

I drove straight to my bank branch in Colorado Springs before going home. In-person verification required ID, signature, and a fraud affidavit. I signed it calmly. I requested a full transaction history for the past 12 months. The branch manager didn’t dramatize anything. She printed documents. She highlighted the unauthorized attempts. She explained the escalation path.

“It’s good you came in immediately,” she said. “It wasn’t luck. It was structure.”

When I pulled into my driveway, the house looked hollow. No dining table through the front window. No rug. No patio chairs. The front door opened easily. They hadn’t changed the locks.

Inside, the silence was heavy, but not shocking. The living room was stripped. Wall mounts remained where the television had been. The cedar chest was gone. My father’s photo from my commissioning ceremony was gone. That part hit, not because of monetary value, because of choice. They chose what to take.

I walked room to room, photographing everything. Every empty bracket. Every missing appliance. The safe in my bedroom was open exactly as it appeared on camera. The $800 emergency cash was gone. Under the bottom shelf of the safe, taped flat, was an index card I had placed there months ago. It read: Check the account names.

I peeled it off and slipped it into my pocket. I didn’t leave it as a trap. I left it as confirmation.

Downstairs, my phone rang again. Lauren. I answered this time. Her voice was strained.

“They’re saying the funds are under investigation,” she said. “The rental office wants verification.”

“That makes sense,” I replied.

“You’re going to ruin everything.”

“No,” I said. “I’m protecting my name.”

There was breathing on the other end. Not yelling, not insults, just calculation. Then she asked, slower this time, “Where is the rest of it?”

I looked around the empty room. “You’re looking at what you thought was everything,” I said.

And I ended the call.

I set my bag down in the middle of the empty living room and called the Colorado Springs Police Department’s non-emergency line. Not because I wanted sirens. Not because I wanted someone in handcuffs. I wanted a report number.

The dispatcher transferred me to property crimes. I explained that while I was out of state on official duty, unauthorized individuals removed property from my home and attempted a large wire transfer from my bank account. I didn’t dramatize it. I listed facts.

They asked if there was forced entry. No. Were the individuals known to me? Yes. Did I have documentation? Yes.

That changed the tone immediately.

An officer arrived within the hour. Mid-40s. Calm. Notebook in hand. He walked through the house slowly while I pointed out missing items: television, laptop, jewelry box, the cedar chest, several framed photos, kitchen appliances, even the spare microwave from the garage. He took photos. He asked for the camera footage. I showed him the clips from that morning: Lauren directing movers, my mother carrying boxes, the safe being opened. He didn’t react visibly, but he nodded once.

“You said they emailed you about this?” he asked.

I pulled up the message and handed him my phone. He read it silently. “They admitted removal of property,” he said. “That’s helpful.”

Helpful isn’t the word most people expect in that situation. But in legal terms, helpful means clear.

He gave me a case number. He said a detective would likely follow up within a few days because there was an interstate financial component. He said it could involve coordination with banking investigators. Still no drama, just paperwork.

After he left, I walked into what used to be Lauren’s room. The closet was empty. Hangers gone. Dresser gone. The indentation in the carpet where her bed had been was still visible.

Four years. Four years of covering bills while she reset.

I pulled up the bank portal again. Status update: the initial $63,000 transfer remained under hold at the receiving bank, pending fraud verification. The second attempt had been fully blocked. A third attempt appeared in the log, initiated but immediately declined due to account restriction. She had tried again after I ended the last call.

The pattern was clear. She wasn’t acting on emotion. She was acting on urgency.

My phone buzzed. Fraud investigations outbound call. I stepped outside to answer. The investigator confirmed they had contacted the receiving institution in Hawaii. The account there was in Lauren’s name. Funds were partially frozen pending documentation.

“If law enforcement provided a case number, it would strengthen the hold,” he said.

I gave him the report number.

He also asked whether anyone in my household had prior authorized access credentials. No. Any written agreement that could be interpreted as shared ownership? No.

“Then, from our perspective, this is unauthorized access.”

That sentence mattered more than any apology I would never receive.

An hour later, my mother called. Her tone was different now. Not sharp. Not defensive. Strained.

“The rental office says they need proof of cleared funds,” she said.

“I’m not providing that.”

“We already moved in.”

“That was your decision.”

She sighed heavily. “Lauren thought…”

“I know what she thought.”

Silence.

“You’ve always had more than enough,” she said finally.

That sentence hit harder than anything else so far.

More than enough.

As if savings accumulated over 12 years of service were a family surplus.

“It’s not shared property,” I said.

“You’re her sister, and that’s supposed to mean what?”

She didn’t answer directly. She never does. Instead, she pivoted.

“This doesn’t need to get ugly.”

“It already was.”

I ended the call and went back inside. The house echoed now. My footsteps sounded louder without furniture absorbing the noise. I opened the garage. The extra refrigerator was gone. The power tools were gone. Even the spare folding chairs were gone. They hadn’t left anything of convenience.

I sat on the floor in the empty living room and began making a list, item by item, estimated value, purchase year, not for anger, for insurance.

Then I opened my laptop and logged into my Army email. Before rumors or background checks could complicate anything, I needed to control the narrative inside my unit. I drafted a brief message to my security manager requesting a meeting regarding a personal financial fraud issue that had resulted in an open police report. I attached the bank fraud case number and confirmed I had initiated the report voluntarily. Transparency matters in the military. I didn’t mention Hawaii. I didn’t mention family drama. I mentioned unauthorized financial access and protective steps taken.

Send.

Within 15 minutes, I received a response acknowledging receipt and asking me to bring documentation the next morning.

Good.

Back to the bank portal. The status on the $63,000 had shifted again: temporarily credited, provisional adjustment. That meant the bank had issued a provisional credit back to my account while the investigation continued. The rest of the attempted $487,000 never left.

Lauren had believed she drained my entire account. In reality, she had managed to move less than 15% before the system locked her out.

My phone rang again. Lauren.

I answered.

“You froze everything,” she said.

“No, the bank did.”

“You moved the real money.”

“I secured my finances.”

“You’re making this criminal,” she said.

“It already is.”

Her breathing tightened. “You could just authorize it. We could split it. No one needs to know.”

That was the first explicit admission. Split it.

“You don’t get to negotiate with money that isn’t yours,” I said.

“You’re overreacting.”

I stood up and walked into the kitchen. The cabinets were open and half empty. They’d even taken the coffee maker.

“No,” I said. “I’m reacting appropriately.”

There was a long pause. Then she said, quieter this time, “The rental office says if the funds don’t clear, they’ll cancel the lease.”

“That’s between you and them.”

“You’d let that happen?”

I looked at the empty counter where my coffee maker used to sit. “Yes,” I said.

I slept on the floor that night with my back against the wall where my couch used to be. Not because I had to. Because I wanted to hear everything. The house felt different without furniture. Sound carried. Every shift in the air felt amplified.

Around midnight, my phone buzzed again. Lauren. I didn’t answer. She left a voicemail this time. Her voice was sharp at first, then shaky. She said the rental office had officially notified them that the lease would not activate until verified funds cleared. She said the property manager mentioned fraud flags. She said I was humiliating them.

Humiliating them.

I stared at the ceiling and let the words sit there.

The next morning, I drove straight to Fort Carson before stopping anywhere else. I had an 08:30 meeting with the security manager, uniform pressed, documentation folder in hand. He didn’t look surprised when I laid everything out: fraud-alert timeline, unauthorized wire attempts, police report number, bank correspondence.

He reviewed it carefully. “You initiated reporting immediately?” he asked.

“Yes.”

“You notified the bank before funds cleared?”

“Yes.”

“You voluntarily disclosed to us?”

“Yes.”

He nodded once. “This doesn’t read as financial irresponsibility. It reads as someone attempting unauthorized access.”

That distinction mattered.

He explained the standard process. A note would be entered in my file indicating a reported fraud incident with documentation attached. As long as I remained cooperative and no adverse findings emerged against me, there would be no clearance impact. He closed the folder.

“You handled this correctly.”

It wasn’t praise. It was acknowledgment.

Outside the building, my phone buzzed again. Unknown Hawaii number. I answered.

“This is Michael from Island Crest Rentals,” the man said. “We have a lease agreement tied to funds currently under investigation. Are you Captain Natalie Brooks?”

“Yes.”

“We were informed the transfer may have been unauthorized.”

“That’s correct.”

“Do you authorize any portion of that transaction for release?”

“No.”

There was a brief silence. “Understood,” he said. “We will proceed accordingly.”

Proceed accordingly meant the lease would collapse if alternate funds weren’t provided.

I ended the call and walked toward my car. Lauren called less than five minutes later.

“What did you tell them?” she demanded.

“The truth.”

“You’re ruining everything.”

“You signed a lease assuming you could take half a million dollars without permission.”

“It wasn’t taking. It was family.”

“No,” I said. “It wasn’t.”

She shifted tactics. “We can pay you back,” she said quickly. “Just let this clear. We’ll send it back once we’re stable.”

That argument works on people who believe promises without structure.

“You don’t get unsecured loans from me,” I said.

“You’re being cold.”

I almost laughed at that. Cold is moving someone’s money across state lines without asking.

She went quiet for a second. Then she asked something new.

“Did you plan this?”

That was interesting.

“Plan what?”

“To trap us.”

I leaned against my car and let out a slow breath. “I didn’t set a trap. I lowered limits. I enabled alerts. I required confirmation. Basic financial hygiene. If you attempt something you’re not authorized to do, the system responds.”

“You knew we were leaving.”

“I knew you were asking questions.”

She hung up.

By early afternoon, I received confirmation from my bank that the provisional credit had been formally posted. The $63,000 was back in my account, pending final resolution. The remaining attempted transfer never moved. The fraud case was now formally escalated to an internal investigative team coordinating with the receiving bank.

The detective from Property Crimes called later that day. He asked for a copy of the email and the video footage. I sent both. He confirmed that because the financial component crossed state lines, coordination with federal banking regulations would apply, but the primary theft case would remain local unless prosecutors chose otherwise. He didn’t promise charges. He didn’t threaten arrest. He said documentation was strong.

Strong is better than loud.

That evening, I walked through the house again with a legal pad. I updated the inventory list. I photographed empty shelves in the garage. I measured the space where my father’s cedar chest used to sit. I opened the closet in my bedroom and noticed something new. A small folder was missing. Inside that folder had been copies of older bank statements and insurance documents. Nothing recent, nothing that gave access, but enough to suggest they had been gathering information for months.

That part confirmed intent more than the wire attempts.

I texted my attorney and let him know about the missing documents.

Add it to the file, he replied.

At 7:40 p.m., my mother called. Her voice sounded tired now.

“The rental office canceled the lease,” she said. “I’m not surprised. Lauren is trying to find another place.”

“With what?”

Silence.

“We thought you’d understand,” she said quietly.

“Understand what?”

“That you have more than you need.”

There it was again. More than I need. As if service pay and disciplined investing were excess inventory in a warehouse.

“I have what I earned,” I said.

“She’s your sister.”

“And I’m not her bank.”

My mother exhaled slowly. “She said you moved the real money before she could access it.”

“I secured my accounts.”

“She thinks you were watching her.”

I looked around the empty living room.

“I was,” I said.

Another silence. Then she asked, almost cautiously, “How much did she actually get?”

I didn’t answer immediately, because the truth wasn’t just a number, and she was finally starting to understand that.

I locked the front door behind me and drove back to base with the windows down even though it was cold. I needed air, not to calm down, to think clearly. The money was mostly secure. The police report was active. The bank had escalated the case. But the part that could quietly wreck everything wasn’t Hawaii. It was my clearance.

Financial irregularities get flagged. Large transfers. Fraud investigations. Police involvement. Even if you’re the victim, the system doesn’t assume that automatically. It checks.

By 9:00 the next morning, I was back in my security manager’s office with updated documentation. He had already reviewed the initial report I filed the day before. Now, I handed him the bank’s provisional credit notice, confirmation of the freeze, and the detective’s contact information. He flipped through each page methodically.

“Any outstanding debt?” he asked.

“No.”

“Any joint financial entanglements?”

“No.”

“Any undisclosed accounts?”

“No.”

“Have you lost control of your primary funds?”

“No.”

That last one mattered. Losing money doesn’t cost you a clearance. Losing control does.

He leaned back slightly. “From what I see, you identified suspicious behavior, implemented safeguards, and reported the incident immediately. That works in your favor.”

“Will this trigger a review?” I asked.

“It will be annotated,” he said. “That’s standard. But annotation isn’t punishment. It’s transparency.”

Transparency is a currency in the military. Hide something and you’re in trouble. Document it and you’re fine.

As I stood to leave, he added one more thing. “Keep all communication in writing where possible. Avoid verbal escalation.”

That advice wasn’t just professional. It was practical.

Back at my office, I checked my phone. Three missed calls from Lauren. One voicemail. I played it. Her voice was steadier now, controlled.

“We’re working with a different rental company,” she said. “We just need a few days. If you could release part of it, just enough for the deposit, we can handle the rest.”

Release part of it, as if this were a negotiation over a used car.

I didn’t call back. Instead, I emailed my attorney and attached the voicemail file.

Attempt to solicit partial release after fraud flag, I wrote in the subject line.

He replied within the hour. Do not engage in conditional release discussions. Maintain position.

Maintain position. It sounded like something from a field manual.

Around noon, the detective called again. He had reviewed the camera footage in full.

“The video shows them directing removal of property,” he said. “Combined with the email and the attempted transfer, that supports unauthorized taking.”

“Are charges likely?” I asked.

“Too early to say,” he replied. “We’ll forward findings to the district attorney’s office once documentation is complete.”

Measured. Not dramatic.

He asked whether I had any written communication where Lauren acknowledged the money wasn’t hers. I forwarded screenshots of texts where she referred to splitting it and asked why I had moved the real money.

Intent doesn’t always shout. Sometimes it whispers in word choice.

After I hung up, I received an email notification from my bank’s fraud investigations team. The receiving institution in Hawaii had confirmed that the $63,000 had been placed under extended hold due to the originating bank’s formal fraud affidavit and the police case number.

Translation: Lauren couldn’t touch it.

By 1500, my commander asked me to step into his office. He closed the door but didn’t sit behind the desk. He stood by the window instead.

“I’ve been briefed that you reported a financial fraud issue,” he said.

“Yes, sir.”

“You comfortable sharing the broad outline?”

“Yes, sir.”

I kept it clinical. Unauthorized access attempts by family members while I was TDY. Protective measures in place prior to incident. Immediate reporting to bank, law enforcement, and security office.

He listened without interruption.

“You anticipate any financial hardship from this?” he asked.

“No, sir.”

“Any leverage point someone could exploit?”

“No, sir.”

He nodded once. “Then handle it. Keep it documented and keep your focus here.”

That was it. No lecture. No suspicion. Just expectation.

Outside his office, my phone buzzed again. This time it was my mother. I answered. Her voice sounded smaller than it had before.

“Lauren says you’re turning this into a criminal case.”

“I filed a police report because property was removed and money was accessed without authorization.”

“She didn’t mean to steal.”

“She meant to transfer nearly half a million dollars. She thought you’d agree.”

“She didn’t ask.”

There was a long pause. “She says the bank is calling it wire fraud,” my mother added quietly.

“That’s what it is.”

The word landed differently when I said it out loud. Fraud isn’t a dramatic word. It’s a technical one. It describes behavior without emotion attached.

“She’s scared,” my mother said.

I leaned back in my chair. “She should be.”

Another silence. Then she asked the question she had been circling around.

“Are you going to press charges?”

I didn’t answer immediately, because the truth was I hadn’t made that decision yet. The system was already moving. My choice wasn’t whether to create consequences. It was whether to escalate them.

“I’m cooperating with the investigation,” I said finally.

That was accurate.

After the call ended, I opened my email again. Promotion board results were scheduled for release within weeks. Timing matters in everything. An unresolved financial investigation tied to your name, even as a victim, can complicate perception. But perception bends toward documentation.

My bank portal refreshed automatically. The status on the held funds had updated again: funds secured, investigation ongoing.

Secured. That word felt solid.

Lauren called again before the end of the duty day. I let it ring. A text followed.

You’re choosing money over family.

I stared at the screen for a few seconds before responding.

No, I typed. I’m choosing accountability.

I put the phone down and returned to the report I had been drafting for work. Deadlines don’t pause for family drama, and neither does the Army.

I forwarded the final batch of screenshots to the detective before shutting down my computer for the night. By that point, everything existed in three places: my email, my attorney’s file, and the police case folder.

Redundancy isn’t paranoia. It’s protection.

The detective assigned to the case, Lorraine Castillo, called two days later. Her voice was direct and unhurried.

“We’ve reviewed the footage and communications,” she said. “I’d like to confirm a few timeline points.”

I pulled up my notes.

Moving truck arrival: 8:52 a.m.

First wire attempt: 6:58 a.m.

Second attempt: 10:16 a.m.

Third attempt: 4:11 p.m.

“All initiated from your residential IP,” she said. “And no written authorization exists.”

“Correct.”

“Your mother’s email indicates knowledge of the transfer.”

“Yes.”

“That helps establish awareness.”

Awareness matters. It separates confusion from intent.

She also confirmed something else. The receiving bank in Hawaii had flagged the incoming $63,000 not only because of my fraud affidavit, but because Lauren had called them twice asking when the funds would clear. She had identified herself as the recipient. She had asked whether holds could be expedited. Those calls were logged.

Desperation creates records.

Lorraine asked whether I had given Lauren or my mother any financial authority in writing at any point. I hadn’t. No joint accounts. No notarized documents. No shared ownership agreements. She explained the likely path forward. Her department would submit findings to the district attorney’s office. Given the documented attempts, the interstate nature of the wire, and the recorded admissions in email and voicemail, the case met thresholds for potential charges.

She didn’t promise an arrest. She didn’t need to.

After I hung up, I checked my bank portal again.

Final fraud determination: unauthorized transaction confirmed. Funds permanently reversed.

The $63,000 was officially restored. The remainder had never left. Lauren had drained nothing. The only thing she managed to move was furniture.

Later that afternoon, my attorney called. “The bank’s determination strengthens everything,” he said. “Now we shift from defensive to civil recovery.”

Civil recovery. That meant restitution.

Insurance had already processed a preliminary claim based on my inventory list and photos. The adjuster walked through the house two days earlier, nodding at empty spaces and taking notes. Replacement-value coverage doesn’t replace memory, but it replaces items. Between the bank’s reversal and the insurance payout estimate, I had recovered most of the financial damage.

But civil recovery wasn’t about money at that point. It was about record.

Lauren called again that evening. Her tone had changed completely. No anger. No accusation. Controlled.

“I spoke to a lawyer,” she said.

“That’s smart.”

“They said this could escalate.”

“Yes.”

“You don’t have to do this.”

“I didn’t initiate anything.”

“You filed a report.”

“Yes.”

“You froze the money.”

“The bank did.”

She paused. “If this goes to court, it affects everyone.”

“It already does.”

There was a shift in her voice. “What if we agree to pay back anything the insurance doesn’t cover?”

“You already tried to take it.”

“We thought…”

“I know what you thought.”

Silence again.

She tried a different angle. “Mom’s really upset.”

“I’m aware.”

“You could drop the complaint.”

“I’m cooperating with law enforcement.”

“That’s a yes.”

“It’s a statement of fact.”

She exhaled sharply. “You moved the real money before we had a chance.”

That line again. Chance.

I leaned against the kitchen counter, which still had no coffee maker on it.

“You had no chance,” I said. “Because it was never yours.”

She didn’t respond immediately. Then she asked, quieter this time, “Did you really think we’d steal from you?”

I didn’t hesitate.

“Yes.”

And that was the part she hadn’t anticipated. Not the frozen transfer. Not the bank hold. Not the police report. The expectation.

Back at work, I continued preparing for the upcoming promotion board. My officer evaluation report cycle had just closed. Performance metrics were solid. Deployment leadership evaluations were strong. But perception matters in leadership pipelines. An unresolved criminal investigation tied to your name, even as a victim, can introduce noise.

So I kept everything transparent. I sent my commander an update summarizing the bank’s final determination and the detective’s status review. No drama, just facts. He replied with a short acknowledgment: Continue mission focus.

That’s the Army’s version of emotional support.

Three days later, Lorraine called again.

“The district attorney’s office is reviewing the case,” she said. “They’re considering formal charges related to attempted theft and wire fraud.”

I closed my office door before responding. “What are the options?”

“Potentially criminal filing,” she said. “Or negotiation of a restitution agreement before filing.”

Restitution agreement. Structured repayment. Avoidance of formal prosecution in exchange for compliance.

I understood the implications. Criminal filing would create a public record, possible arrest warrant, and long-term consequences. Restitution would still require admission of unauthorized action, but could prevent escalation.

My attorney called an hour later.

“They’ve reached out,” he said. “Lauren retained counsel. They’re exploring settlement.”

Of course they were. Once banks label something fraud and detectives start building timelines, the word family loses protective power. Settlement meant acknowledgement. It meant paperwork. It meant admission without courtroom theatrics.

That night, I walked through the house again. The insurance adjuster’s tape markers still dotted the floor where larger items had been documented. The space felt less shocking now. Empty doesn’t mean destroyed. It means available.

My phone buzzed once more. Lauren. I let it ring. A text followed.

Is this really worth it?

I typed back slowly.

Yes.

I reviewed the draft settlement agreement at my kitchen counter, which was still the only flat surface left in the house. Lauren’s attorney had sent it over that morning. The document didn’t use emotional language. It used structured repayment terms, acknowledgement of unauthorized access, and a clause requiring full cooperation with ongoing banking and law-enforcement reviews.

In exchange, the district attorney’s office would consider suspending formal criminal filing contingent on compliance.

Translation: pay it back, follow the rules, and avoid a courtroom.

My attorney walked me through every paragraph over speakerphone. “Do not focus on the apology language,” he said. “Focus on enforceability.”

The proposed terms included repayment of any insurance deductible I incurred, structured reimbursement for items not fully covered by insurance, formal acknowledgement that the wire-transfer attempts were unauthorized, a five-year repayment schedule secured by automatic drafts, and immediate reactivation of criminal filing if a single payment was missed. No handshake. No family understanding. Legal obligation.

“Does she have income?” I asked.

“Her attorney claims she secured remote work,” he said. “Enough to sustain the repayment plan.”

Hawaii didn’t last long. Once the rental lease collapsed and the receiving bank account was frozen, Lauren and my mother relocated again. Not back to Colorado. Not yet. Somewhere cheaper. Consequences don’t always arrive dramatically. Sometimes they show up as relocation notices and canceled leases.

I signed the agreement after one final revision clarifying that restitution did not equal forgiveness. Paper doesn’t forgive. It enforces.

The district attorney’s office confirmed conditional suspension of criminal charges upon filing of the executed agreement. The detective called me personally to confirm.

“If she defaults, we file,” she said.

“Understood.”

That was it.

Seven months had passed since the morning in D.C. In those months, I replaced furniture one piece at a time. I didn’t rush. I chose deliberately. A new dining table. A different couch, not the same model as before. I wasn’t recreating what was taken. I was rebuilding differently.

Insurance covered most of the tangible losses. The bank fully restored the attempted wire. Between insurance and the reversal, roughly 88% of the financial disruption was resolved. Real life doesn’t give you 100% back. It gives you most of it and leaves a dent. The dent was manageable.

Two weeks after the settlement was finalized, the Army released promotion-board results. The email came through midmorning. Subject line: FY promotion board results. I closed my office door before opening it.

Selected for major.

No ceremony. No confetti. Just a line of text with my name on it.

That mattered more than the money. Not because rank is everything, but because it meant the incident had not contaminated my record. My documentation, transparency, and timing had worked.

I stepped outside and called my mom. She answered on the second ring.

“I was selected,” I said.

There was a pause. “That’s good,” she replied quietly.

No enthusiasm. No celebration. Just acknowledgement.

“Lauren signed the agreement,” she added. “She says she’ll make the payments.”

“That’s between her and the contract,” I said.

“She feels like you chose your career over family.”

I leaned against the railing outside the building. “I chose accountability.”

“She says you could have handled it privately.”

“I did. I handled it through the proper channels.”

Silence again.

“You’ve changed,” my mother said.

“No,” I replied. “I haven’t.”

After I hung up, I looked down at my phone and noticed something small. No missed calls from Lauren. For the first time in months, there were none.

At home that evening, I sat at my new dining table with a laptop open in front of me. The house felt different. Not empty anymore. Just quieter. The first automatic restitution payment posted to my account the following week. It wasn’t a large amount. It wasn’t symbolic. It was scheduled. Consistency matters more than size.

My attorney confirmed that as long as payments continued and no new violations occurred, the criminal filing would remain suspended. If she defaulted, the agreement would collapse and charges would move forward. Clear. Measurable. Structured.

At work, nothing changed outwardly. Same deadlines. Same training schedules. Same expectations. But internally, something had shifted. I wasn’t carrying uncertainty anymore.

Lauren texted once after the first payment cleared.

I hope this is enough.

I responded with a single sentence.

It’s a start.

Not emotional. Not forgiving. Just accurate.

Later that night, I walked into the spare bedroom that used to belong to her. I had turned it into a home office. Standing desk. Dual monitors. Filing cabinet. Order. I opened the bottom drawer and placed a copy of the settlement agreement inside, behind my updated insurance documents and bank correspondence. Not as a trophy. As a reminder.

Accountability isn’t loud. It doesn’t shout. It doesn’t humiliate. It simply exists and waits for compliance.

My phone buzzed one more time before I went to bed. A message from my mother.

Do you think we’ll ever go back to normal?

I stared at the screen for a few seconds.

Normal had been four years of covering expenses and ignoring red flags. Normal had been assuming that because I was stable, I was available.

I typed slowly.

Normal wasn’t working.

Then I put the phone down on the nightstand and turned off the light.

I let the phone ring twice before answering. The number still had a Hawaii area code, even though I knew they weren’t in Hawaii anymore.

“Hi,” my mom said. No accusation. No edge. Just a small word.

I stepped out onto my back patio and closed the door behind me. The Colorado air was cold and dry, the kind that clears your head without asking permission.

“How are you?” she asked.

“I’m fine.”

There was a long pause, the kind where someone is deciding how honest they’re willing to be.

“Lauren made the second payment,” my mom said. “On time. I saw. She’s trying.”

I knew that part was true. The automatic drafts were coming in exactly as outlined in the agreement. Not large. Not dramatic. But consistent.

“She says she feels like you’re punishing her,” my mom continued.

I leaned against the railing. “She attempted to move half a million dollars without authorization.”

“She didn’t think of it that way.”

“That’s the problem.”

Another silence.

“I keep thinking about that morning,” my mom said. “The email.”

“So do I.”

“I shouldn’t have written it like that.”

“No,” I agreed.

She exhaled slowly. “We thought you had more than enough,” she said again, softer this time.

I didn’t respond immediately. I had heard that phrase enough.

“More than enough doesn’t mean available,” I said.

“I see that now.”

I didn’t argue with her. Recognition doesn’t need correction.

The wind shifted slightly. Somewhere down the block, a dog barked. Ordinary sounds. Normal neighborhood life.

“Do you think we’ll ever get back to how things were?” she asked.

I thought about that. How things were meant I paid the mortgage while Lauren rotated through ideas. It meant my savings were considered communal insurance. It meant small boundary crossings that added up over time.

“I don’t want to go back,” I said.

She was quiet for a long moment. “What does that mean?”

“It means we move forward differently.”

“How?”

“No shared accounts. No financial assumptions. No emergency access without written agreement.”

“That sounds formal.”

“It is.”

Another pause.

“Lauren feels like you don’t trust her.”

“I don’t.”

The word landed cleanly. Not loud. Not angry. Just accurate.

“She says you were watching her.”

“I was.”

“That hurts.”

“So does wire fraud.”

I didn’t say it to be sharp. I said it because it was the right word.

She didn’t argue this time.

“She didn’t think you’d actually go to the police,” my mom admitted.

“I know.”

“She thought you’d handle it privately.”

“I did. Through the system.”

Silence again.

“You’ve always been different,” she said. “More structured.”

“That’s how I built what I have.”

“And that’s why she thought you’d be okay.”

There it was. The underlying logic. Strong equals absorbent. Responsible equals flexible. Disciplined equals forgiving.

“That assumption is what got us here,” I said.

The wind picked up again. I could hear papers shifting slightly inside through the patio door.

“She misses you,” my mom said.

“I’m not gone.”

“It feels like you are.”

“I’m not available the way I used to be.”

Another long pause.

“Would you ever visit?” she asked.

“Maybe.”

Maybe. It wasn’t a promise. It wasn’t a rejection. It was space.

“I don’t want this to define us,” she said quietly.

“It already does,” I replied. “We just decide what it defines.”

We stood in silence on opposite ends of the country. She finally spoke again.

“She asked me to tell you something.”

I waited.

“She said she didn’t think you’d outthink her.”

I let out a small breath that might have been a laugh. “This wasn’t about outthinking anyone. It feels like it.”

“It was about protecting myself.”

“She thinks you set her up.”

“No,” I said. “I set boundaries. There’s a difference. If someone attempts to access money that isn’t theirs and the bank stops them, that isn’t a trap. It’s a system working as designed.”

“She doesn’t know how to come back from this,” my mom said.

“She doesn’t need to come back to where we were,” I replied. “She needs to stay current on the agreement. That’s the only thing that matters now.”

The restitution payments continued on schedule. Automatic drafts, logged and timestamped. No missed months. No partial deposits. Consistency changes narratives.

Over time, the calls became less frequent. Not hostile. Not emotional. Just shorter.

At work, life moved forward. New responsibilities as a major. Larger scope. More oversight. Promotion didn’t change who I was. It confirmed it.

One evening, months later, I sat at my dining table reviewing budget projections for the next fiscal year. My phone buzzed once. Lauren. I considered letting it go to voicemail, then answered.

Her voice was calm. “I made the payment,” she said.

“I saw.”

“I’m not asking for anything.”

“Okay.”

There was a pause.

“I was wrong,” she said finally.

The words didn’t come with explanation. They didn’t come with defense. Just a statement.

“I know,” I replied.

Silence again.

“I didn’t think you’d enforce it,” she added.

“I did.”

She exhaled slowly. “Yeah.”

That was the entire conversation.

After we hung up, I sat there for a moment, looking at the room around me. Different couch. Different table. Same house.

They thought love meant I wouldn’t enforce what was mine. They thought being the responsible one meant absorbing loss quietly. They were wrong.

And that realization didn’t feel loud. It felt steady.

I didn’t lose my family over money. I lost the version of myself that believed responsibility meant silent sacrifice. What happened wasn’t just family drama. It was a line being crossed. And once you see a line clearly, you can’t pretend it was never there.

My sister drained my $500,000 account because she believed I wouldn’t enforce boundaries. She believed being strong meant being flexible. She believed love meant access.

It doesn’t.

This wasn’t about revenge in the dramatic sense. It was about accountability. Real family revenge stories aren’t about screaming or public humiliation. They’re about documentation, patience, and letting systems work. They’re about protecting your career, your name, and the life you built.

I didn’t destroy my family. I stopped financing it.

If this story resonated with you, if you’ve ever dealt with family betrayal, financial boundaries, or toxic family dynamics, subscribe to the channel. I share real revenge stories and family revenge stories that are grounded, realistic, and rooted in discipline, not drama.

There’s a difference between being cold and being clear.

News

I Was 45 Minutes Late With a Delivery—Then I Saw a Red Child’s Shoe Under an Executive Desk

The day I was forty-five minutes late for my delivery, the millionaire female CEO on that floor looked at me but didn’t raise her voice. A single cold sentence was enough to make me understand I was wrong. I signed…

I Came Home From My Walk And Found My Wife Sitting In Silence. Our Daughter Said She Had Only Stopped By To Check On Her. Later, An Old Recording Made Me See That Visit Very Differently.

I came home from my morning walk and found my wife sitting at the kitchen table, perfectly still, staring at nothing, not reading, not drinking her coffee, just sitting there like a woman who had forgotten how to exist inside…

My Daughter Moved Me Into a Care Facility and Said, “That’s Where You Belong.” I Didn’t Fight in the Moment. That Night, I Started Checking the Paperwork.

My daughter secretly sold my house and put me in a nursing home. “That’s where you belong.” I nodded and made one phone call. The next morning, she came to me trembling and in tears. In her hands, she was…

My Longtime Bookkeeper Emailed Me Just Before Midnight: “Walter, Call Me Now.” By The Time My Son Set The Papers In Front Of Me, I Knew Someone Had Been Using My Name Without My Knowledge.

The email came at 11:47 on a Tuesday night, and I almost didn’t see it. I had been sitting at the kitchen table in my house in Asheville, North Carolina, going through a stack of old seed catalogs that Margaret…

Three Weeks Before I Planned To Tell My Son I Was In Love Again, A Nurse At Mercy General Pulled Me Aside And I Realized People Were Making Plans About My Life Without Me

Formatted – Beatrice & Fern Story Three weeks before I planned to tell my son I was in love again, I walked into Mercy General for a routine cardiology appointment, and a woman I barely recognized saved my life. I…

At A Washington Fundraiser, My Son’s Fiancée Smiled And Called Me “The Help.” I Said Nothing, Went Back To My Hotel, And Started Removing Myself From The Parts Of Her Life That Had Only Ever Looked Independent From A Distance.

At a political gala, my future daughter-in-law introduced me as the help. My own son said nothing. So that same night, I quietly shut down the campaign, the penthouse, and every dollar funding her self-made lie. By morning, everything she…

End of content

No more pages to load